TITLE : FAQ on FDI in Korea 2023 (Q57~Q60)

페이지 정보

본문

■ FAQ on FDI in Korea 2023 (Q51~Q56)

Establishment of Corporation

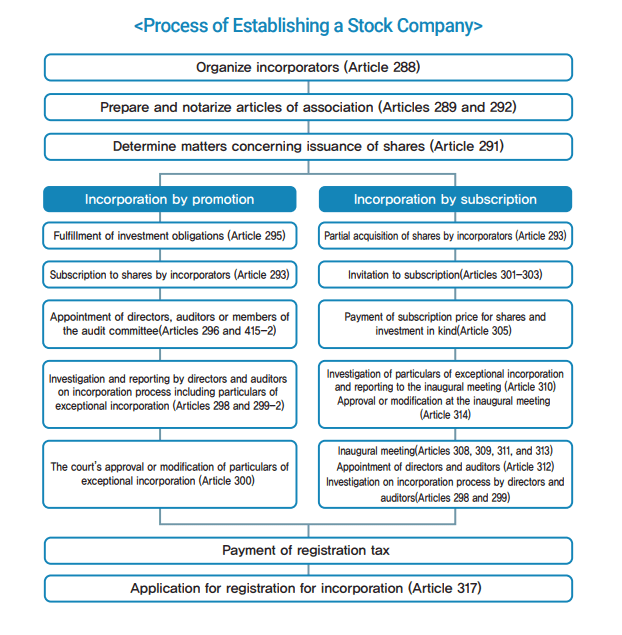

Q57 What is the process of establishing a corporation in Korea?

A57 There are four types of corporations - general partnership company,limited partnership company, stock company, limited companyand limited liability company – that can be established underthe Commercial Act of Korea. As a stock company represents anabsolute majority, the process of establishing a stock company isexplained below (the “Act” refers to the Commercial Act).

Q58 What are the differences between an individual business and a corporation?

A58

- Differences in terms of nature of business

- An individual business: An individual engages in business under his/her name and has full ownership of the business as well as unlimitedliability for business debts.

- A corporation: A corporation is an entity completely different fromindividuals, and its operation is run by the representative directorunder the name of the corporation. A corporation limits its liabilityand guarantee to the amount of its assets and the representativedirector, directors and shareholders that are the members of thecorporation are not liable to its debts.

- Differences in terms of establishment procedures

- An individual business: An individual business can carry out businessafter notifying foreign investment and receiving a certificate ofbusiness registration from the competent tax office, withoutadditional procedures.

- A corporation: A corporation is required to undergo incorporationprocedures (incorporation registration, business registration) andthe process may take around two more weeks due to documentpreparations and procedural matters for registration.

| Individual Business | Corporate Business | |

| Applicable laws | Income Tax Act | Corporate Tax Act |

| Taxable income | Tax owed for only for theincome in the relevant year | Tax owed for businessincome and liquidated incomeof each business year |

| Obligation of taxpayment | Tax owed for only for theincome in the relevant year | Tax owed for businessincome and liquidated incomeof each business year |

| Tax rates | 6-45%* | 9-24% |

| Fiscal year | The taxable period isdetermined so that tax onincome earned from January1 to December 31 of eachyear can be paid pursuant tothe Income Tax Act | The business year can bedecided arbitrarily by thearticles of association |

| Obligation ofbookkeeping | Only individual businessesof a certain size or larger areobligated to prepare financialstatements | Every corporation isobligated to prepare financialstatements |

| Subject of rightsand obligations | The owner of an individualbusiness is the subject ofall and any of the rights andobligations related to theprofit-generating activities ofthe individual business. Thebusiness can be attributed tothe owner’s income, but theowner becomes a directlyinvolved party to a default,etc. and assumes unlimitedliability. | The responsibility of investorsis limited to the amountof their investment exceptotherwise prescribed in theCommercial Act |

| Use of property | Profits earned from businessbelong to the business owneras an individual | Profits earned from businessprimarily belong to thecorporation |

* If the tax base is not high according to the tax rate table, an individualbusiness has an advantage in tax payment, but if the taxable income isabove a certain threshold, a corporate business is at an advantage. Anindividual business may save taxes if it transitions to a corporation.

Q59 What are the advantages of establishing a domestic branch vs. establishing a foreign-invested company?

A59

- A domestic branch of a foreign company (branch office or liaison office)

- Establishing a branch is relatively simple, as capital is not required andonly the necessary expenses can be remitted.

- For operating income, corporate tax should be paid in Korea, but profitis non-taxable when it is remitted overseas.

- Foreign-invested company (local company)

- A foreign-invested company is treated as a domestic company whenit is incorporated, so when certain conditions are met, it can receivegovernment support as both a foreign-invested company and adomestic company.

- In particular, if the parent company is an SME, the foreign-investedcompany can receive various benefits as a start-up SME such as taxreduction/exemption when certain qualifications are met.

Q60 What are the differences among a local corporation, a branch office and a liaison office?

A60

- A foreign-invested company (a local corporation)

- An investment of at least KRW 100 million per foreign investor isrequired to establish a foreign- invested company under the ForeignInvestment Promotion Act and the Commercial Act.

- A branch office or liaison office of a foreign company

- A branch office: When engaging in a business that generates profits inKorea, it is classified as a “branch office” under the Foreign ExchangeTransactions Act. Because a branch office is a foreign corporation, it isnot recognized as foreign direct investment.

- A liaison office: A liaison office is different from a branch office inthat it does not carry out business that generates profits in Korea, butinstead undertakes “non-sales” activities such as liaison work, marketresearch, research and development activities. Unlike a branch office,a liaison office is assigned a serial number equivalent to a businessregistration number by a competent tax office without a registrationprocess in Korea.

- Domestic company C (or foreign investor A) should apply for registrationof foreign-invested company (Form 17)

- Reason: New foreign investment

- Required documents: Certificate of corporate registration, certificateof business registration, and shareholder register (or documentscertifying the stock transfer

< Foreign-Invested Company vs. Branch Office vs. Liaison Office >

| Foreign-Invested Company | Branch | Liaison Office | |||||||||||

| Applicable laws | Foreign Investment Promotion Act | Foreign Exchange Transactions Act | |||||||||||

| Type of corporation | Domestic corporation | Foreign corporation | |||||||||||

| Company name | No restrictions | Must be identical to that of the headquarters | |||||||||||

| Scope of business activities | No restrictions within the permitted scope | Restricted to the same activities as the head office, within the permitted scope | Not permitted to generate profits and restricted to activities related to establishing business contacts | ||||||||||

| Capital requirement | KRW 100 million or greater | No restrictions | |||||||||||

| Legal liability | Liability limited to the domestic corporation | iability extends to the headquarters | |||||||||||

| Independence | Independent by law | Subordinated to the headquarters | |||||||||||

| Loans in Korea | Possible depending on its credit rating | Almost impossible | Impossible | ||||||||||

| Establishment procedures | 1. Foreign investment notification 2. Registration for incorporation 3. Business registration 4. Registration of foreign-invested company |

1. Notification of branch establishment 2. Court registration 3. Business registration |

1. Notification of branch establishment 2. Registration of serial number |

||||||||||

| Accounting and taxation | Obligation of bookkeeping according to Korean GAAP and external audit for certain conditions | Obligation of bookkeeping according to Korean GAAP, but no obligation of external audit | No bookkeeping obligation | ||||||||||

| Corporate tax rate |

* Local corporate tax equivalent to 10% of the calculated corporate tax amount is separately imposed. |

No obligation to pay corporate tax | |||||||||||

| Taxable income | Total income based on all profits made by the local corporation | Profit from all domestic-source income of local branch is combined. Branch tax applies in some countries | No taxable income | ||||||||||